A plain-language guide to infinite banking and policy access planning

Curious About Infinite Banking? Read This Before You Book.

See what the strategy usually means, why it is usually tied to whole life, where IUL differs, and what to understand before you review options with a licensed insurance agent.

Start Here

Learn the strategy first

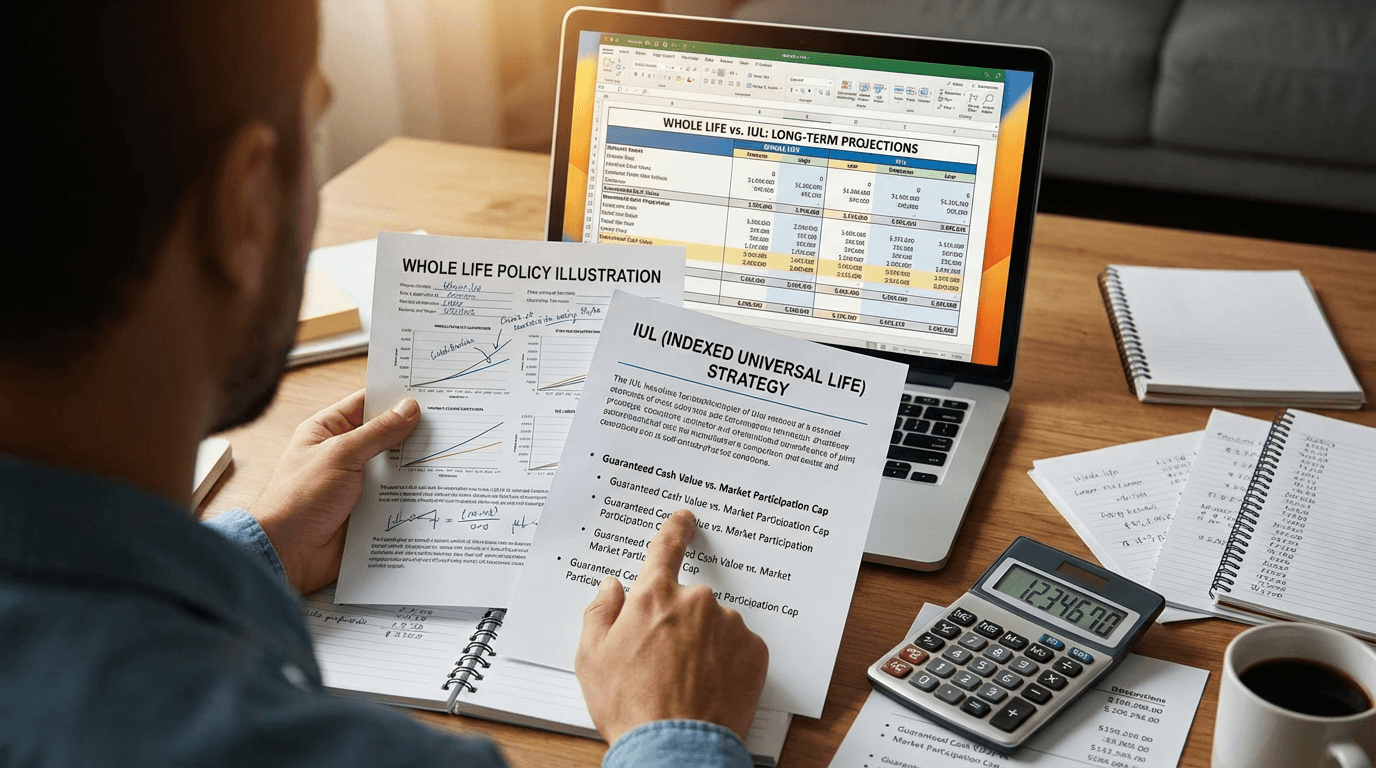

Whole Life vs IUL

See where they differ

Licensed Review

Know the real next step

2,184 readers explored this guide this month

Product disclosure

When this page refers to infinite banking, it is referring to a strategy commonly built with specially designed Whole Life Insurance policies.

This page also shows where IUL may fit, but it does not treat IUL and whole life as the same thing.

Why This Topic Confuses So Many People

Most people do not start by asking for whole life or IUL.

They start because they hear about cash value, policy loans, or more flexibility.

Then they see numbers before they understand the strategy behind them.

They are asked to compare illustrations before they know what product created them.

That is usually where the confusion starts.

Infinite banking is usually built around specially designed whole life.

IUL can play a different role, but it works under different rules.

Budgefy helps you understand that before you decide on a licensed-agent review.

Start with this

“If the product is not clear, the numbers will not be clear either.”

Learn what the strategy usually means, learn where whole life and IUL split, and decide on the review after that.

Why This Page Feels Different

A lot of people are asked to book before they really understand what they are looking at.

This page is built to do the opposite:

Product first — You see what infinite banking usually refers to before anyone asks you to move forward.

Whole life and IUL stay separate — Whole life is the classic setup, and IUL is shown as a different path with different moving parts.

Illustrations stay in their lane — Projections are used to show examples, not to promise an outcome.

Risk stays visible — Loans, lapse risk, and possible tax consequences are stated plainly.

The next step is named — If you move forward, the next step is a review with a licensed insurance agent.

Fit is not assumed — The page does not pretend this makes sense for every person.

What Budgefy can actually show you

Budgefy can organize cash flow, compare funding ranges, and model illustrative timelines. It cannot promise actual policy values, loan access, or tax outcomes, because those depend on product design, funding, carrier assumptions, and whether the policy stays in force.

How It Works: 3 Simple Steps

The first step should feel clear, simple, and easy to follow.

Learn the strategy

See what people usually mean by infinite banking, where whole life fits, and where IUL differs.

Map your numbers in Budgefy

Map your budget, your premium comfort level, your time horizon, and the role borrowing would actually play.

Decide whether to continue

If it still looks relevant, the next step is a review with a licensed insurance agent.

Why People Keep Reading

The goal here is clarity, not hype.

Reader feedback

“It explained why whole life and IUL are not the same thing before pushing me into a call.”

Melissa R.

Wanted product clarity

Reader feedback

“Most pages jump straight to projections. This one made the tradeoffs clear first.”

Jordan C.

Preferred a strategy-first approach

Reader feedback

“The Budgefy angle worked because it connected the strategy to my real budget.”

Andre T.

Needed a fit check first

Strategy-first guide

Illustrative forecasts only

Licensed-agent next step

No obligation to continue

next step

See If This Path Fits

Start with the guide, review the fit, and continue only if a licensed-agent conversation still makes sense.

Educational guide first · No guaranteed outcome