A cash-value life insurance guide with an illustrative policy forecast

See How A Permanent Policy May Build Value Over Time

Estimate premiums, cash value, and possible loan timing before you review permanent coverage options with a licensed insurance agent.

Cash Value

See the long-term path

Loan Timing

Estimate when access may start

Licensed Review

Check fit next

1,928 readers explored this forecast page this month

Forecast disclosure

This page shows illustrative projections only, not guaranteed policy values or guaranteed borrowing results.

If you continue, the next step may be a review with a licensed insurance agent.

Why Permanent Coverage Gets Oversimplified

A lot of people hear about cash value before they hear about the tradeoffs.

They hear borrowing, flexibility, and long-term value.

They do not always hear about charges, time horizon, or lapse risk.

They also do not always hear how IUL differs from term or whole life.

That matters because permanent coverage only makes sense in the right situation.

Budgefy helps you see the moving parts before you review fit with an agent.

See the moving parts

“A projection is useful only when you understand what is driving it.”

Look at funding, time horizon, cash value, and loan timing together instead of looking at a single number in isolation.

Why This Forecast Page Feels Different

Most pages either push permanent life hard or skip the hard parts.

This page keeps the important parts visible:

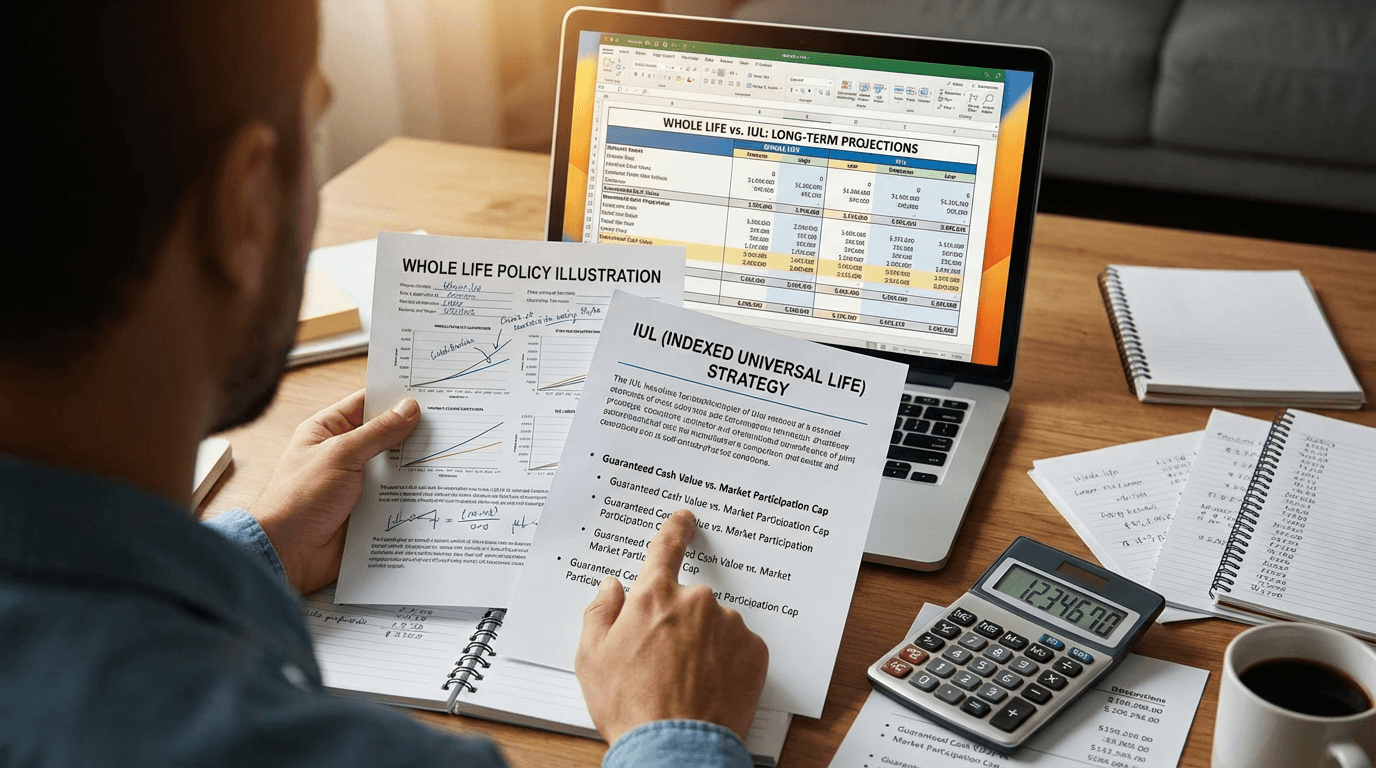

Permanent life is explained first — You see what cash value is and why permanent coverage works differently than term.

IUL is treated as its own product — IUL is not blended into whole life or sold as a one-size-fits-all answer.

Forecasts stay illustrative — Examples are there to help you think, not to promise a future result.

Loans are shown honestly — Policy loans are not free money, and they can affect values and death benefit.

The next step is a review — If you continue, the next step is a licensed-agent review of fit and options.

Tradeoffs stay in the copy — Fees, funding discipline, and lapse risk stay visible instead of being hidden.

What Budgefy can actually show you

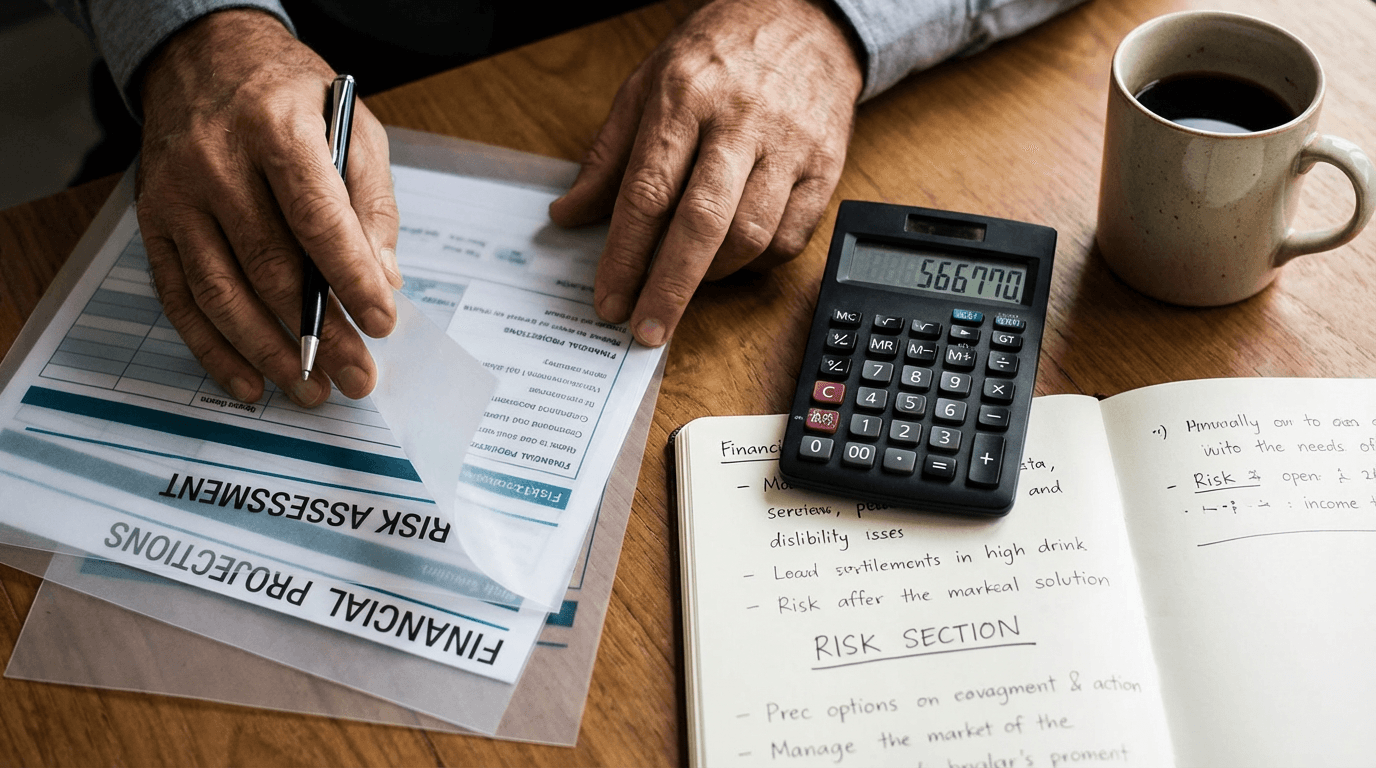

Budgefy can organize cash flow, compare funding ranges, and model illustrative value and borrowing timelines. It cannot promise actual policy values, credited rates, loan access, or tax outcomes, because those depend on product design, funding, fees, carrier assumptions, and whether the policy stays in force.

How It Works: 3 Simple Steps

The first step should make the product easier to understand.

See the product basics

Review what permanent coverage is, what cash value means, and where IUL fits.

Map a sample forecast

Look at premium range, time horizon, projected value, and possible borrowing timing.

Review fit if needed

If it still looks relevant, the next step is a review with a licensed insurance agent.

Why People Keep Exploring

The strongest response to this page should be better product clarity.

Reader feedback

“This was the first page that made permanent life feel understandable instead of mysterious.”

Marcus L.

Wanted a clearer product explanation

Reader feedback

“I liked that it explained cash value and loan timing without pretending the numbers were guaranteed.”

Tiana W.

Preferred a more realistic forecast

Reader feedback

“The Budgefy angle helped because it tied the policy idea back to my real budget and timeline.”

Evan D.

Needed context before speaking with an agent

Permanent-policy explainer

Illustrative forecast only

Loan tradeoffs included

Licensed-agent next step

next step

See A Sample Cash-Value Forecast

Review the product, look at the sample forecast, and continue only if a licensed-agent review still makes sense.

Illustrative forecast first · No guaranteed result